India’s financial institutions are under a new directive: as per the RBI’s communication guidelines and the Telecom Commercial Communications Customer Preference Regulations (TCCCPR), all promotional and service-related calls must originate from the 160 or 140 series number ranges.

The objective is clear and commendable: reduce spam and eliminate scam calls by ensuring that customers only trust calls from designated number series.

To make this effective, Regulated Entities (REs) are expected to educate their customers through awareness campaigns, SMS messages, and ads, explaining that legitimate communication will come only through these registered numbers.

But while this might make sense on paper, the reality is quite different. The effectiveness of this model relies heavily on consumer behavior—and that’s where the cracks begin to show.

Why This Won’t Work in Practice: A Consumer Behavior View

Let’s break down why this scheme may fail to achieve its intended goals:

1. Assumption of Awareness is Flawed

It assumes that consumers will become aware that only 140 and 160 series numbers are legitimate. But the average user is busy, distracted, and not closely tracking the origin of every call they receive. Most simply don’t know what a 140-series number is, and even if told, they may not remember.

2. Consumers Will Still Pick Up Scam Calls

Since the awareness isn’t deeply ingrained, people will continue to answer calls from non-registered numbers. The spam problem will persist because user behavior hasn’t changed.

3. Even Legitimate Calls Get Marked as Spam

Dialer apps like Truecaller allow users to report numbers as spam. If even a small group marks a 140 number as spam, the app may block it for others too. So ironically, compliant financial institutions may still have their calls ignored or rejected.

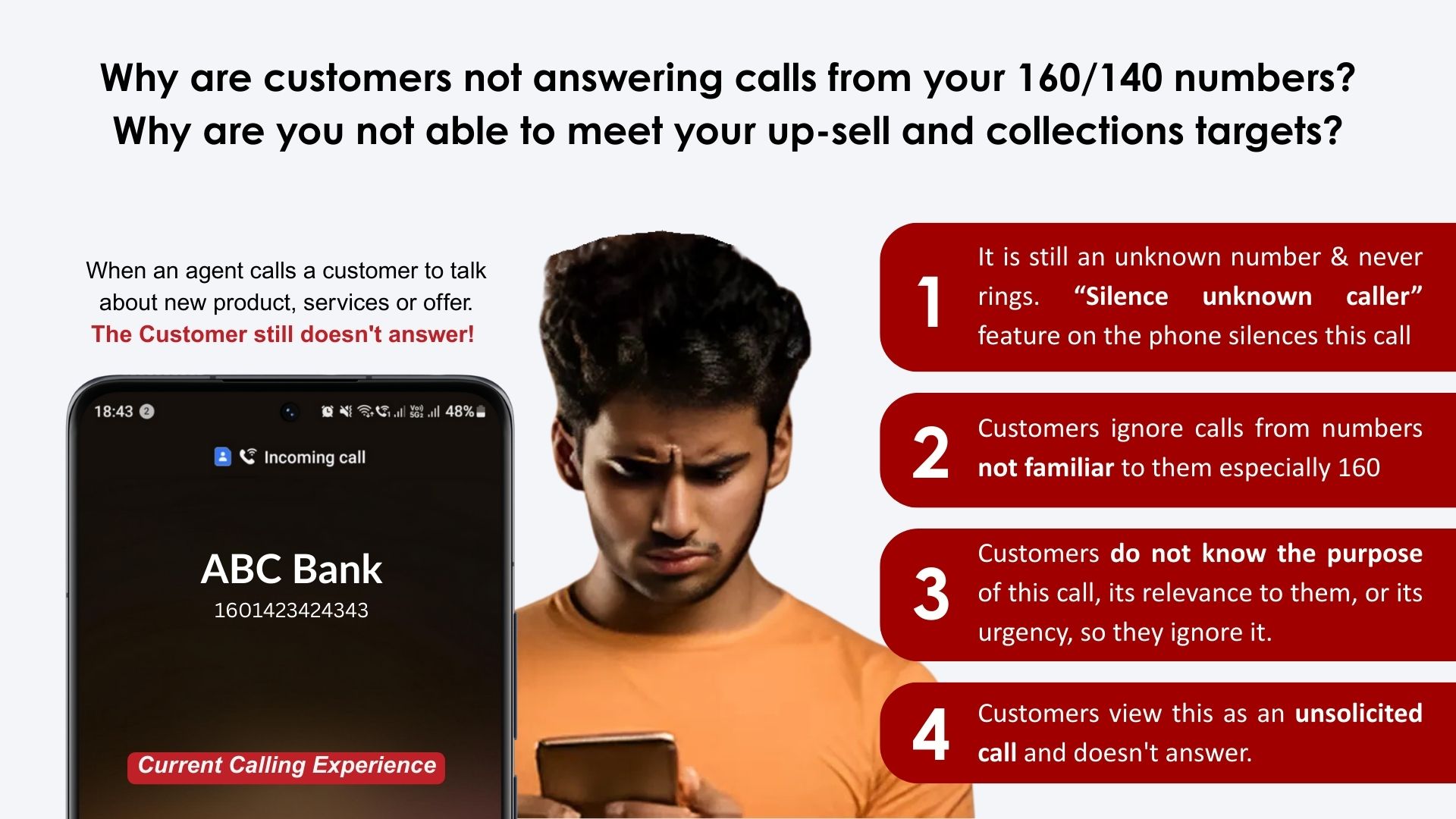

4. Dialer App Settings Block All Unknown Calls

iPhone and Android have a feature called “Block unknown callers” that rejects calls from numbers not saved in the phonebook. A customer who enabled this feature won’t receive any 140 or 160 series calls, including important service notifications.

5. Fails the Customer Experience Test

Every call experience needs to answer three critical customer questions:

- Who is calling me?

- Why are they calling?

- Is this a good time?

The current 140/160 approach fails to answer even one of these. A random 140 number doesn’t tell a customer who’s calling or why. This leads to low trust and low engagement.

6. Incentivizes Workarounds and Plausible Deniability

There’s a risk that some REs might outsource outreach to third-party agencies that skirt the regulations using plausible deniability. We’ve all received calls from agents representing entities with suspicious names like “BajTel,” promising guaranteed returns. If challenged, they claim to be merely lead generators, not the financial entity itself. Meanwhile, the RE benefits from lead generation but denies responsibility for the spam.

The End Result? Bad for Everyone

Financial institutions will suffer from:

- Blocked service and sales calls

- Numbers tagged as spam

- Declining call pickup rates, even among consenting customers

We’re already seeing anecdotal evidence of severely low call pickup rates from 140 series numbers. So what’s the solution?

Assertion Identity Assurance: A Practical Fix for a Broken Model

At Assertion, we recognize that the existing TCCCPR framework needs a usability layer that respects the regulation but improves the customer experience.

Assertion Identity Assurance integrates directly with a financial institution’s app. It enables the following for any customer who has installed the app:

- Branded Caller Identity: When a 140-series call is made to a customer, they see the brand name of the financial institution.

- Contextual Reason for Call: The call screen can show a simple message like: “Update on your FD rates” or “Assistance with loan process.”

- Consent Flow Integration: If required, the app can trigger a consent form that directly registers approval on the DLT (Distributed Ledger Technology) system, ensuring TCCCPR compliance.

This solves the core issues:

- The customer knows who is calling.

- They understand why the call is being made.

- And they are more likely to engage, knowing it’s a trusted source.

Conclusion: A Better Path Forward

While the RBI and TRAI’s intention with the 140 and 160 numbering system is to protect consumers, the strategy’s effectiveness is limited by how real people behave. Without solving for visibility, recognizability, and trust, even compliant REs will suffer from failed outreach.

Assertion Identity Assurance bridges that gap, helping financial institutions maintain compliance while vastly improving customer engagement.

It’s time for financial entities to not only follow the rules but to adopt solutions that make those rules work for them, not against them.